To read the full article as published in Forbes Australia Magazine April/May 2024 Issue, click here ![]() https://www.forbes.com.au/brand-voice/forbes-profile/mortgage-private-credit-ascf/

https://www.forbes.com.au/brand-voice/forbes-profile/mortgage-private-credit-ascf/

Investor’s Update – March 2024

Trading Update

Last months RBA minutes on its decision to leave rates on hold clearly indicate the RBA has adopted a neutral bias in relation to interest rates.

The annual rate of inflation for February remained steady at 3.4% although 0.1% lower than expectations however the unexpected decline in the monthly unemployment rate to 3.7% in February from 4.1% in January shows the labour market may no longer be softening.

ASCF Current Targeted Distribution Rates

ASCF High Yield Fund

| 3 Months | 6 Months | 12 Months | 24 Months |

|---|---|---|---|

| 6.50% | 7.25% | 7.75% | 7.30% |

ASCF Select Income Fund

| 3 Months | 6 Months | 12 Months | 24 Months |

|---|---|---|---|

| 6.25% | 6.75% | 7.25% | 6.75% |

ASCF Premium Capital Fund

| 6 Months | 12 Months | 18 Months | 24 Months |

|---|---|---|---|

| 6.10% | 6.25% | 6.75% | 6.30% |

ASCF Private Fund

| 3 Months | 6 Months | 12 Months | 24 Months |

|---|---|---|---|

| 8.19% | 8.39% | 8.59% | 8.49% |

This was further confirmed by the release of March’s employment data earlier today which came in at 3.8% which was only 0.1% higher than the prior month.

With real GDP growth expanding by a tepid 0.2% in the December quarter February’s lower unemployment rate was certainly a surprise to most economists suggesting there is a disconnect between an economy barely growing and labour market data showing its still running hot.

As a result there remains diverging opinions in relation to how quickly the RBA starts cutting rates, and the recent inflation data print in the US which came in higher than expected has led some to ponder whether we will see an interest rate cut this year at all, suggesting that inflation could be stickier than previously thought.

The Stage 3 tax cuts due to come into force on July 1 will certainly assist with cost of living pressures but the question remains as to whether it will also add pressure to inflation should consumers decide to spend rather than save the additional income.

On balance we believe one should take confidence in the lower GDP number over the unemployment data and our expectation remains that inflation will continue to decline albeit somewhat slower than previously thought allowing the RBA to cut rates later this year.

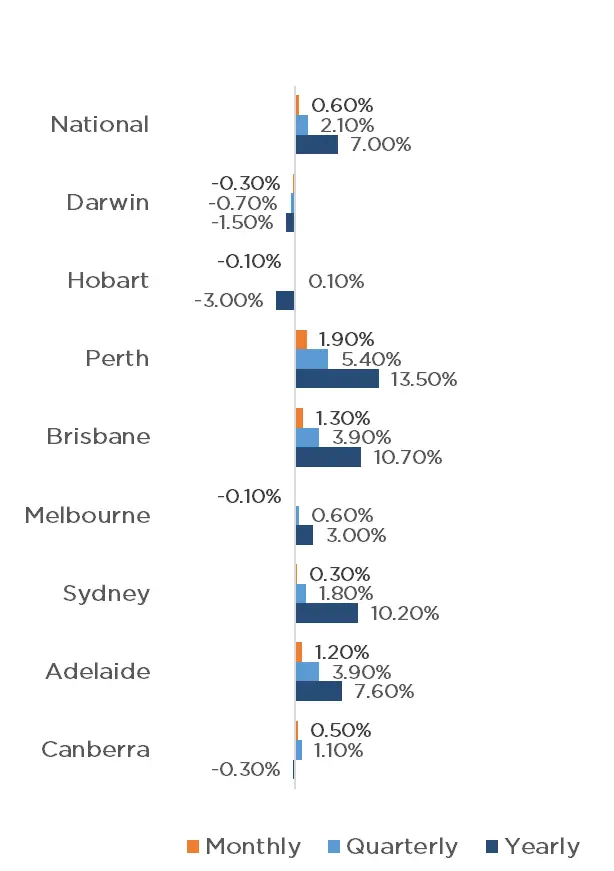

Property prices continued to rise in March with residential property up nationally by 0.6% in March, matching February’s gain.

Half-Yearly Financials Now Online

Our half-yearly audited financial statements for each of our retail funds for the period ending 31 December 2023 are now available for viewing on our website or by clicking here. Should you have any questions, do not hesitate to contact our Investor Relations

team on 1300 269 419.

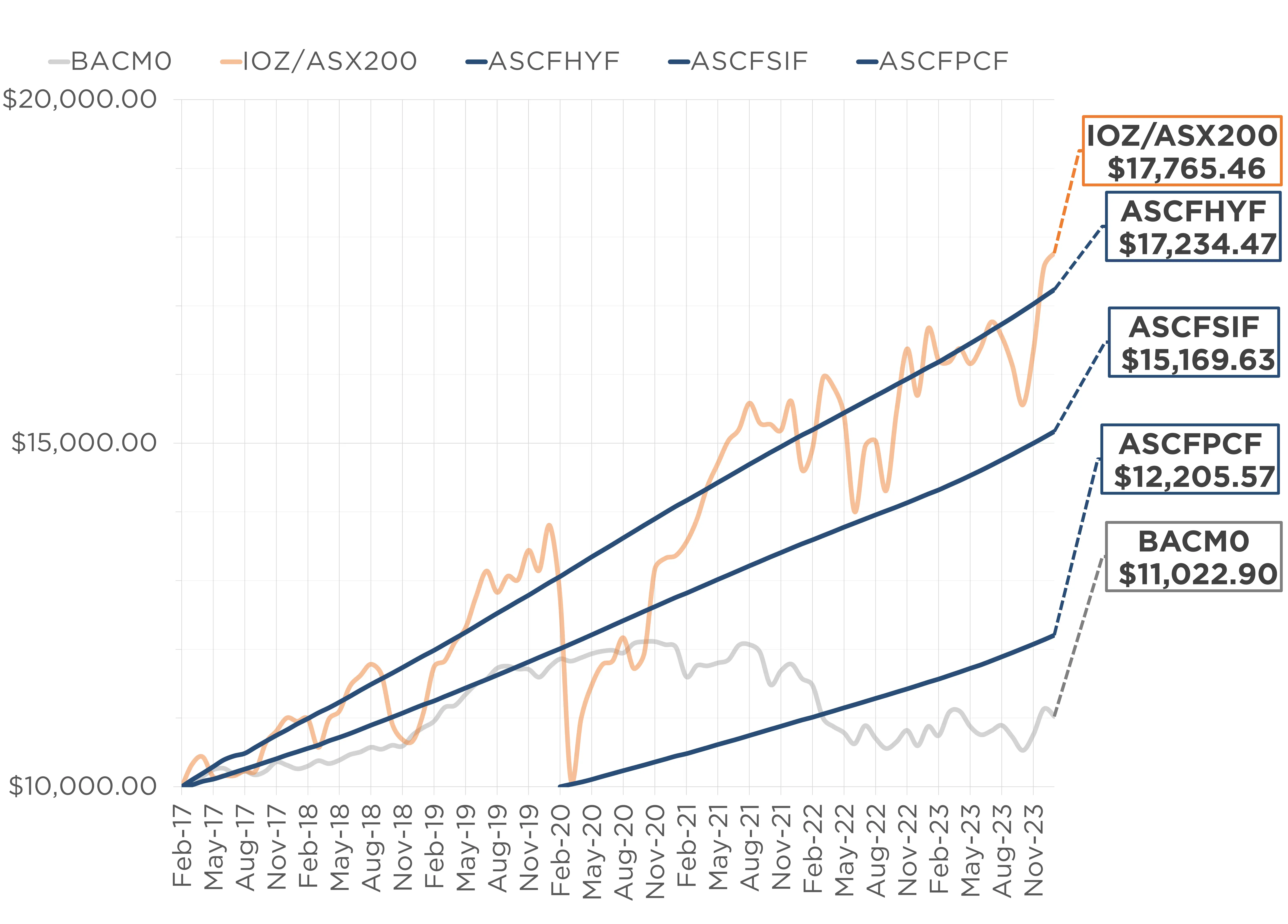

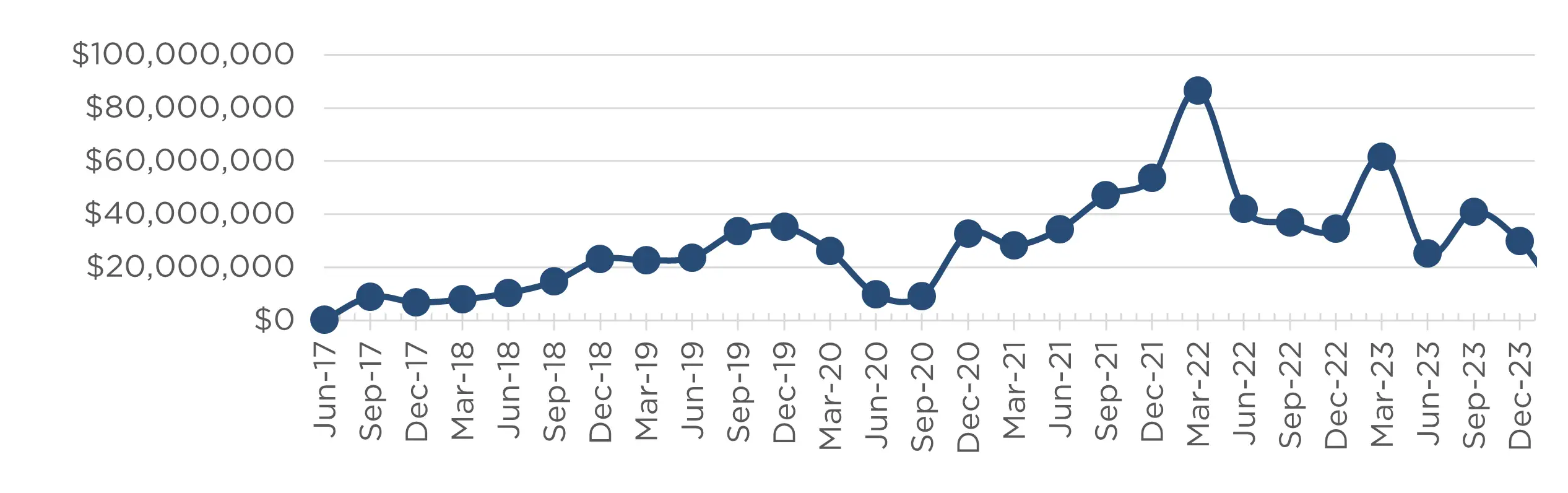

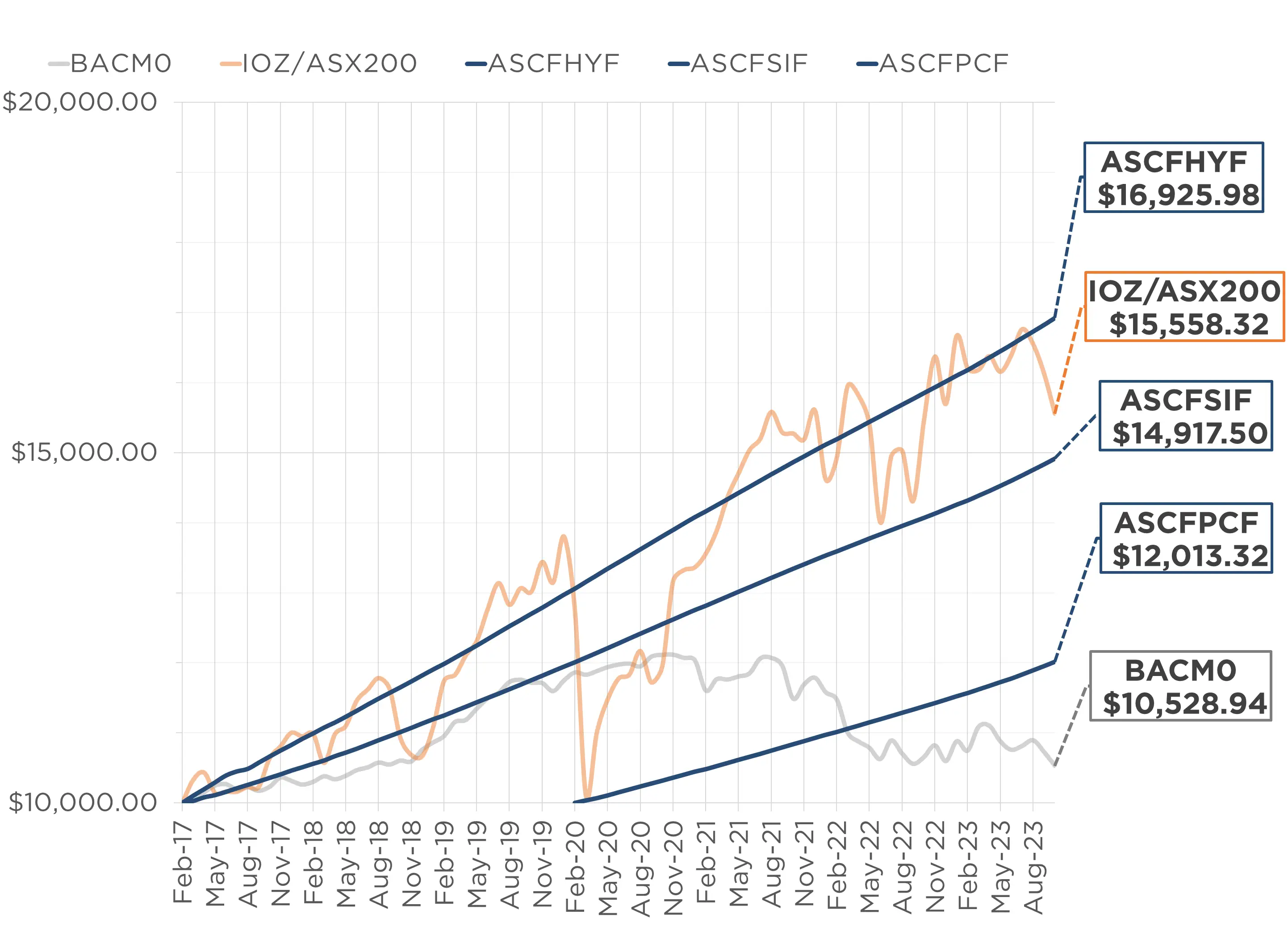

Monthly Managed Fund Cumulative Growth & Performance

Note 2: Past performance is not indicative of future performance

Managed Funds Under Management

as at 31st of March 2024

| March 2024 | |

|---|---|

| ASCF High Yield Fund | $139,923,343.97 |

| ASCF Select Income Fund | $44,792,692.73 |

| ASCF Premium Capital Fund | $23,489,870.02 |

| Combined Funds under Management | $208,205,906.72 |

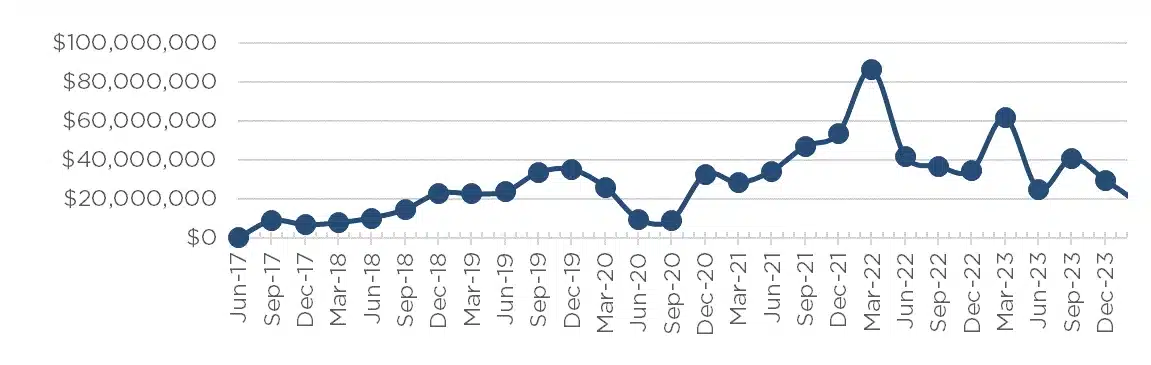

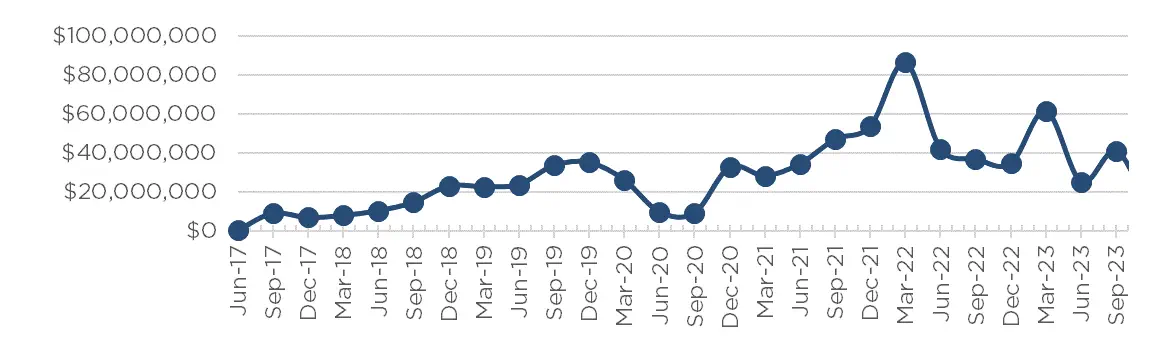

In March, loan originations and inquiry levels remained solid, with $20,856,000 in new loan originations settled.

The unit price across all three of our retail funds remains stable at $1.00 per unit.

All monthly distributions have been paid in full for the month of March.

Lending Activity Update

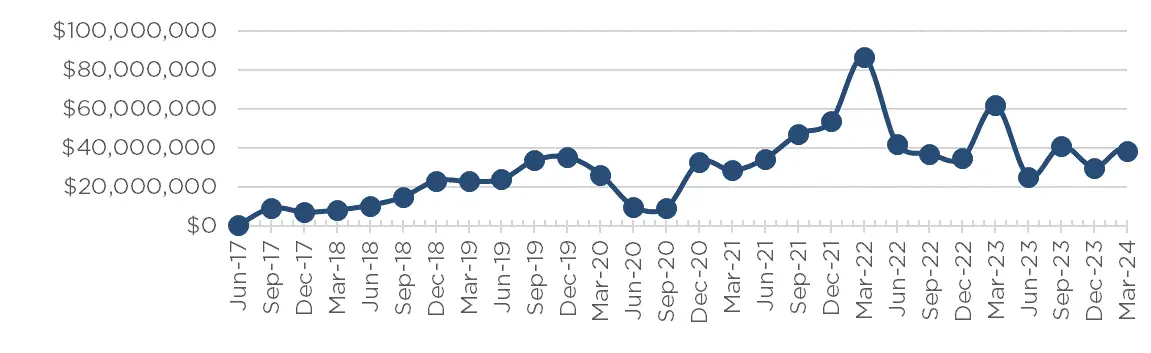

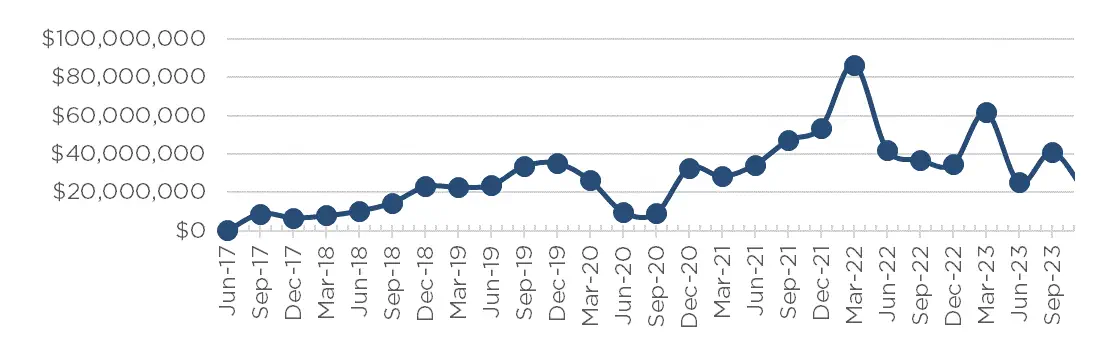

Quarterly Loan Settlements

as at 31st of March 2024

Current Loans by Fund Source

as at 31st of March 2024

| High Yield Fund | Select Income Fund | Premium Capital Fund | |

|---|---|---|---|

| 1st Mortgage Loans | 79.99% | 100% | 100% |

| 2nd Mortgage Loans | 15.79% | 0% | 0% |

| 1st & 2nd Mortgage Loans | 4.22% | 0% | 0% |

| Avg. Weighted LVR | 55.97% | 53.25% | 47.27% |

| Avg. Loan Size | $1,352,262.43 | $1,054,660.33 | $810,822.02 |

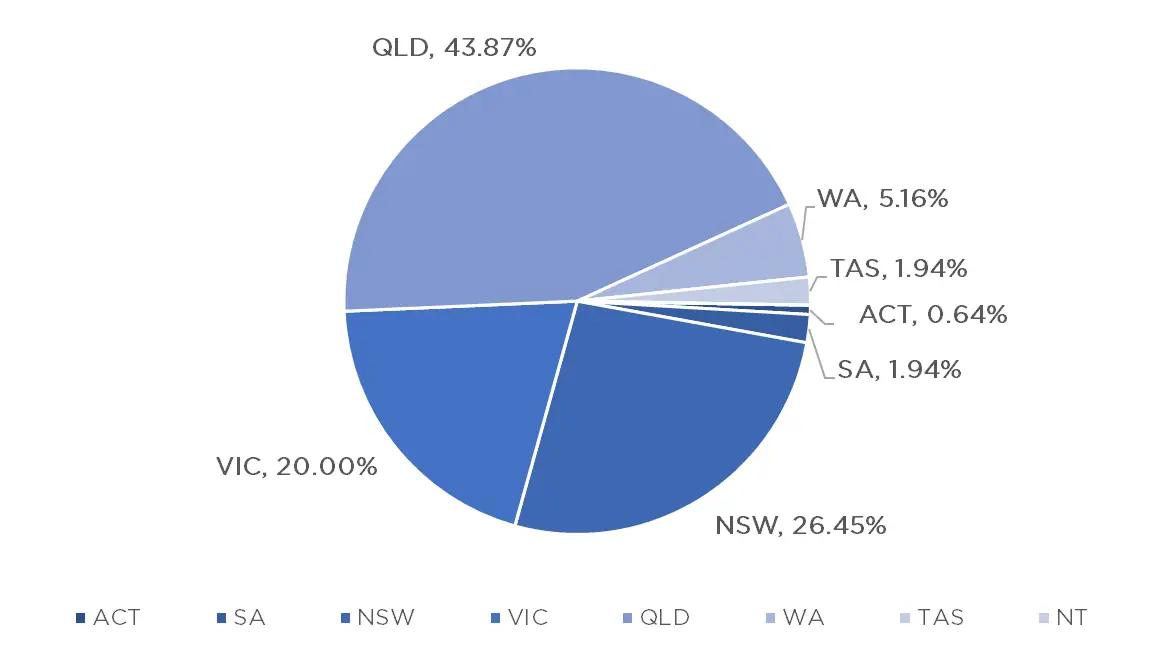

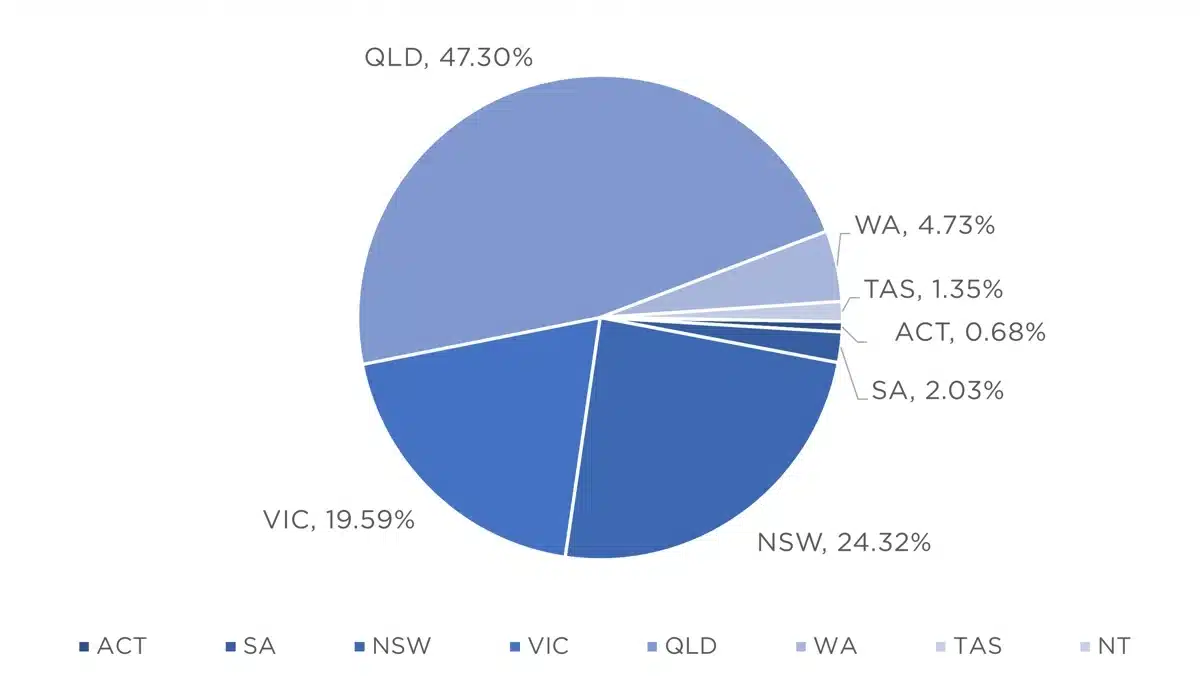

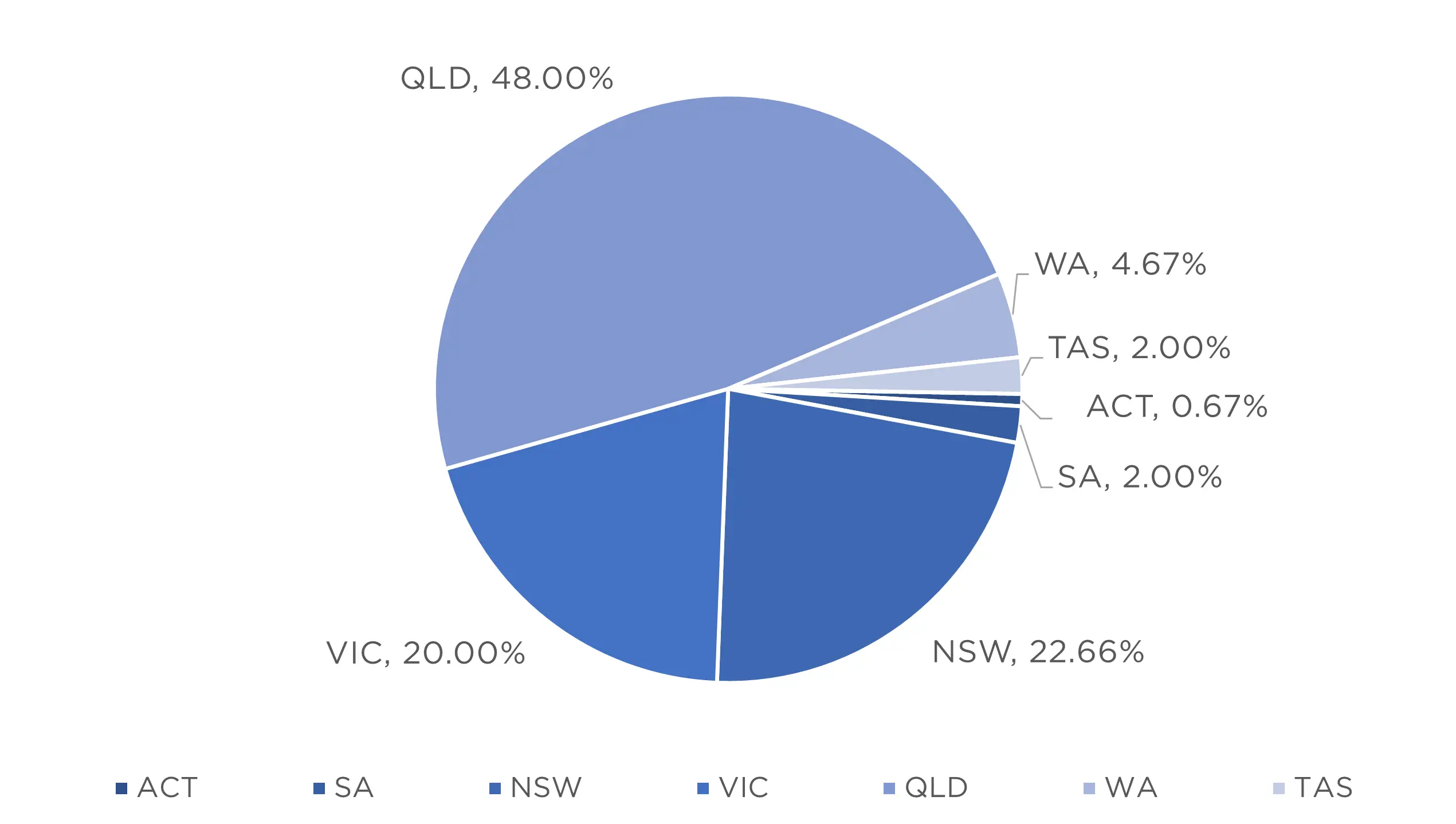

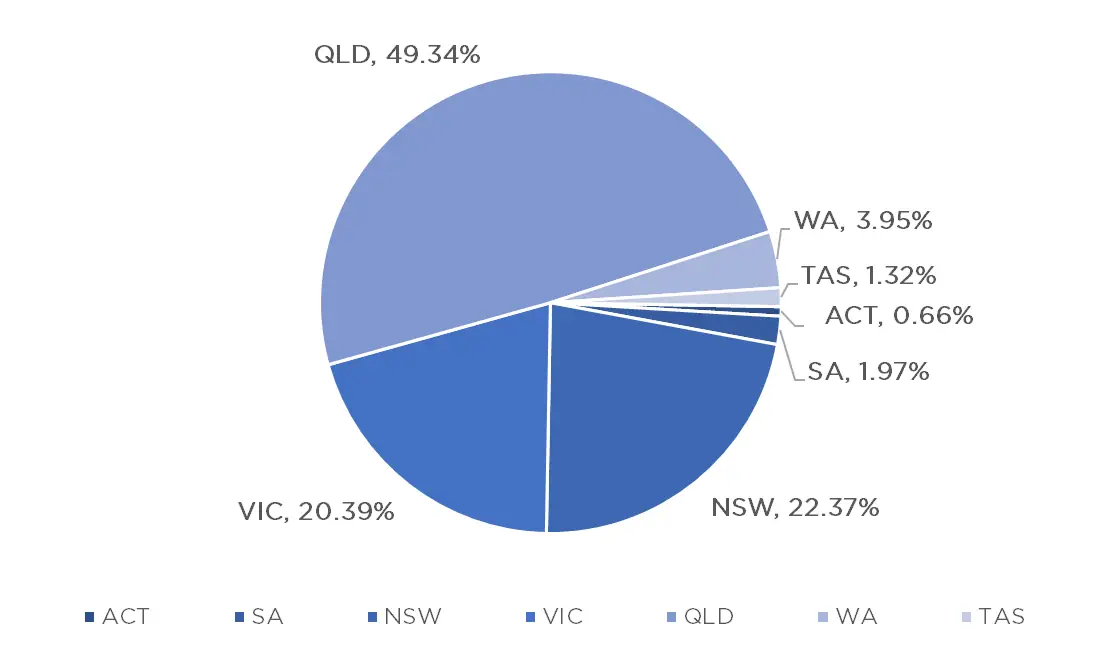

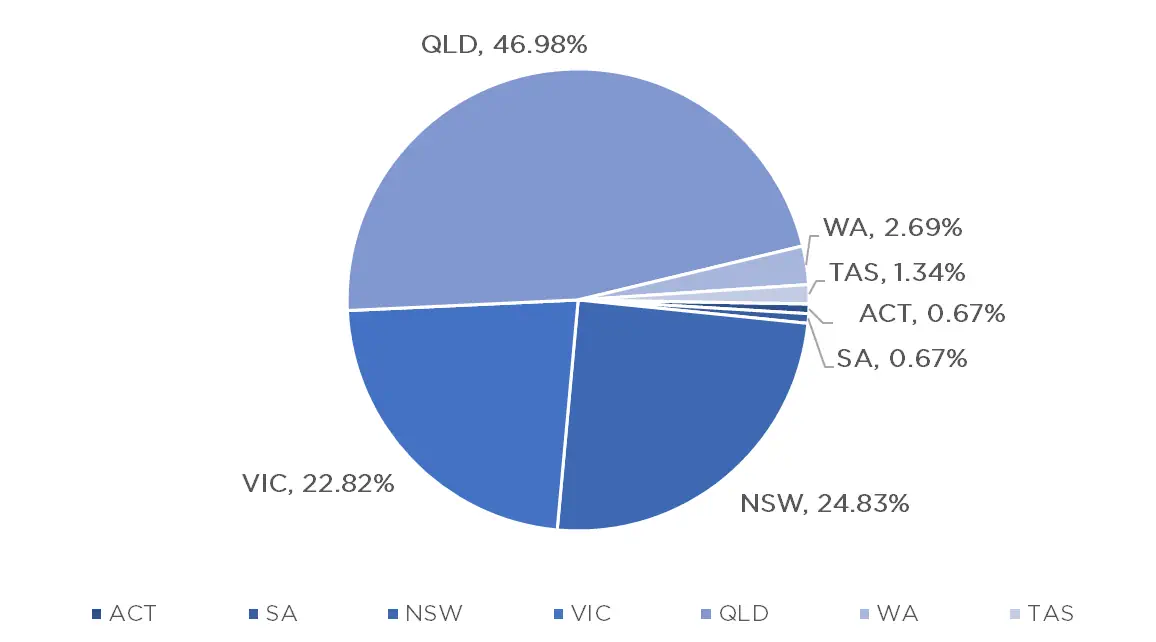

Current Loans Geography

as at 31st of March 2024

Why Invest with ASCF?

Property investment has always been a significant contributor to building wealth in Australia. However, not all investors are able to secure a direct investment in property or perhaps want to manage the issues that arise when dealing with tenants and the ongoing burden of the statutory charges associated with owning a property including payment of rates, land taxes and water levies.

Most non-owner occupier residential property investments in Australia are negatively geared which means they are cash flow negative once the monthly mortgage payment and all statutory expenses associated with holding the property are paid.

This is typically a cash drain on other sources of income and while there may be capital appreciation this is usually not able to be crystallised until the property is sold.

ASCF’s pooled mortgage funds offer an alternative to direct property investments. They offer investors the opportunity to invest in the property market without having to purchase and manage properties themselves.

The funds invest in mortgages over Australian property and offer a targeted distribution return to investors of between 6.1% and 7.75% p.a depending on the fund selected and the investment term.

This makes them an attractive option for those who want to diversify their portfolio and gain indirect exposure to the property market.

In addition, our pooled mortgage funds offer regular income payments in the form of targeted monthly distribution payments, particularly for investors who are seeking an income stream.

Most economists are now expecting the RBA to reduce rates by between 0.25% and 0.75% over the next 12 months so if you are seeking an inflation responsive return that offers a monthly distribution, consider our funds as part of your investment strategy.

An Interesting Transaction

Problem:

A lending scenario was presented to us by one of our valued brokers whereby a customer required $340,000 for 6 months for his security consultancy business to allow him to complete new contracts.

Solution:

The customer was prepared to provide a 2nd mortgage over his principal place of residence to secure the loan resulting in a LVR (including the confirmed 1st mortgage) of 68.12%. ASCF provided a 6 month term loan at an annual interest rate 19.80% after receiving a full valuation from one of our panel valuers.

The loan will be repaid in full once payments for those completed contracts are received from his customers.

What ASCF Does Differently:

Our speed to market was paramount to winning this transaction as the customer required expedient access to capital to engage his suppliers and ensure he had sufficent resources to complete the new contracts. Another reason why customers continue to turn to ASCF to meet their short term funding needs.

Market Update

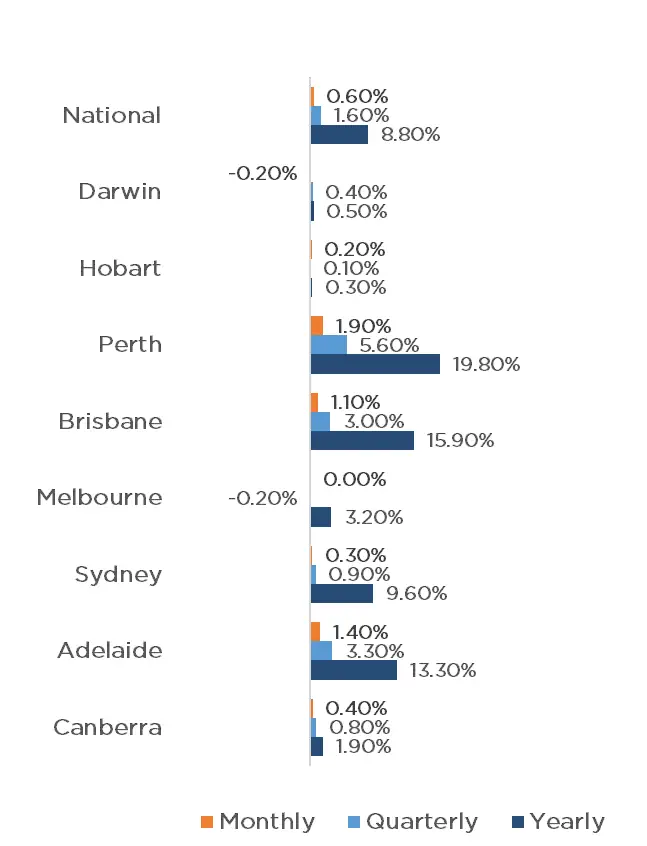

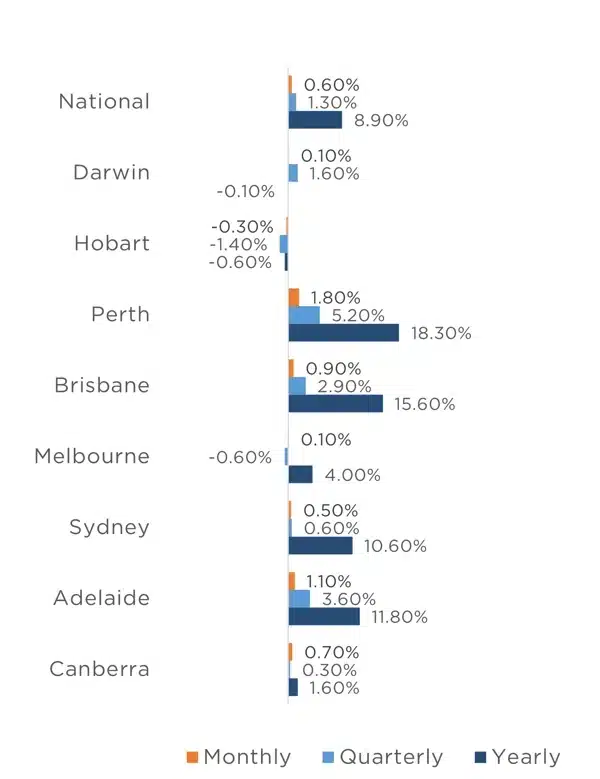

Property values continue to increase across the majority of the country, with CoreLogic’s National Home Value Index recording a further 0.6% increase in March, on par with what was achieved in February, resulting in 14 months of continuous monthly growth. Perth continued to be the strongest performer, increasing by a mammoth 1.9% for the month, followed closely by Adelaide with 1.4% and Brisbane with 1.1%. Signs of cooling have begun in Canberra, Sydney and Hobart, with 0.4%, 0.3% and 0.2% growth respectively. Melbourne achieved parity for the month, whilst Darwin is the only capital to experience a loss, falling by 0.2%. This monthly data contributes to a 1.6% national increase for the quarter, with all capital cities experiencing some level of quarterly growth except for Melbourne, where a 0.2% reduction has occurred.

As we wait for the next RBA meeting, scheduled for the 7th of May, there are growing calls by economists for a rate reduction to occur, driven by the continued slowing of GDP growth and falling inflation. Whether or not a reduction is made in May, it appears all but certain that throughout 2024 there will be reductions, which will likely result in a further bump to property prices in the coming months.

Clearance Rates & Auctions

week of 2nd of April 2024

Property Values

as at 31st of March 2024

Median Dwelling Values

as at 31st of March 2024

Quick Insights

Steadfast Forecast

Oxford Economics Australia, a leading economic institute has forecasted median property to grow to almost $2 million in Sydney alone within the next 3 years.

“You have a fundamentally undersupplied market and with net overseas migration running at half a million people, a growing participation by foreign buyers, downsizers and cash buyers, demand has outweighed that drag that interest rates would typically have.”, said Maree Kilroy, Oxford Economics senior economist.

Source: Australian Financial Review

Affordability is the Trend

The medium-high end of the Sydney housing market may have finally reached a peak that lower end buyers cannot afford as a flood of homebuyers move into previously affordable suburbs driving prices up.

The lower end market has grown 5 times as fast as the higher end in past 6 months, and is likely to continue as more people seek to delay the effect of the housing crisis in their lives.

Source: Australian Financial Review

Investor’s Update – February 2024

Trading Update

The release of the GDP data by the Australian Bureau of Statistics last week which came in at 0.2% for the 3 months to December clearly shows that the impact of the rate rises we saw last year are starting to bite. Annual growth has now slowed to 1.5% from 2.1% in the prior quarter and is the lowest since 2000 if you exclude the pandemic data sets.

ASCF Current Targeted Distribution Rates

ASCF High Yield Fund

| 3 Months | 6 Months | 12 Months | 24 Months |

|---|---|---|---|

| 6.50% | 7.25% | 7.75% | 7.30% |

ASCF Select Income Fund

| 3 Months | 6 Months | 12 Months | 24 Months |

|---|---|---|---|

| 6.25% | 6.75% | 7.25% | 6.75% |

ASCF Premium Capital Fund

| 6 Months | 12 Months | 18 Months | 24 Months |

|---|---|---|---|

| 6.10% | 6.25% | 6.75% | 6.30% |

ASCF Private Fund

| 3 Months | 6 Months | 12 Months | 24 Months |

|---|---|---|---|

| 8.19% | 8.39% | 8.59% | 8.49% |

Monthly inflation data for January came in at 3.4% and based on the weak economic growth number will continue to trend lower. Property prices have mostly stabilised in Melbourne but continue to rise across the other capital cities.

The rental crisis also appears to be getting worse with rents continuing to climb across the country by 0.9% in February and by 8.5% over the last 12 months. So where does that leave our economy? Well with anaemic economic growth and inflation likely to hit the RBA’s target later this year interest rates will come down, with economists divided between one rate cut and as many as three so the cash rate is likely to be somewhere around 3.85% by year end.

The housing crisis is unlikely to see any relief until governments at all levels realise the issue is really one of supply. The policies governments at all levels have implemented historically through stamp duty relief and first home owners grants whilst important do nothing to increase supply levels to make housing more affordable on a sustained basis. Governments need to start removing the red tape on housing approvals, release more land for housing either through new large scale releases or zoning changes as well as incentivise employers in the construction industry to employ more skilled labour.

It is only when they realise that the issue rests on the supply side and take action to increase supply that they can truly start to tackle the housing affordability crisis. This really requires collaboration between governments at all levels nationally and even if they started to work on this immediately it would take at least a couple of years for the benefits of these policies to flow through and make an impact. As a consequence, residential property prices are likely to remain well supported and depending on how much the Federal government tinkers with migration levels between now and year end we expect further price increases are likely as rate cuts start to flow through.

Half-Yearly Financials Now Online

Our half-yearly audited financial statements for each of our retail funds for the period ending 31 December 2023 are now available for viewing on our website or by clicking here. Should you have any questions, do not hesitate to contact our Investor Relations

team on 1300 269 419.

New Staff Appointment

We are pleased to advise that we have recently appointed Mr John Reghenzani as our new Head of Compliance. Mr. Reghenzani has over 25 years experience across the Australian financial services industry spanning roles in private legal practice, as a Senior lawyer at the Australian Securities and Investments Commission and working in-house as a compliance manager and advisor to ASIC regulated managed investment, asset management and retail and wholesale banking businesses.

Mr Reghenzani has a Bachelor of Economics and Bachelor of Laws from Monash University and a Master of Laws from the University of Queensland.

Mr Reghenzani reports to and works with the ASCF Compliance Committee and ASCF Credit Committees in order to support compliance with ASCF’s Australian Financial Services and Australian Credit licenses and associated regulatory requirements.

Monthly Managed Fund Cumulative Growth & Performance

Note 2: Past performance is not indicative of future performance

Managed Funds Under Management

as at 29th of February 2024

| February 2024 | |

|---|---|

| ASCF High Yield Fund | $135,559,793.97 |

| ASCF Select Income Fund | $44,831,687.73 |

| ASCF Premium Capital Fund | $23,334,851.53 |

| Combined Funds under Management | $203,726,333.23 |

In February, loan originations and inquiry levels remained solid, with $9,384,275 in new loan originations settled.

The unit price across all three of our retail funds remains stable at $1.00 per unit.

All monthly distributions have been paid in full for the month of February.

Lending Activity Update

Quarterly Loan Settlements

as at 29th of February 2024

Current Loans by Fund Source

as at 29th of February 2024

| High Yield Fund | Select Income Fund | Premium Capital Fund | |

|---|---|---|---|

| 1st Mortgage Loans | 81.65% | 100% | 100% |

| 2nd Mortgage Loans | 11.75% | 0% | 0% |

| 1st & 2nd Mortgage Loans | 6.60% | 0% | 0% |

| Avg. Weighted LVR | 53.74% | 54.29% | 46.48% |

| Avg. Loan Size | $1,393,290.66 | $1,029,808.36 | $756,388.89 |

Current Loans Geography

as at 29th of February 2024

Why Invest with ASCF?

We are often asked how funds invested in ASCF are secured.

The short answer is that all funds are invested in loans over Australian property secured by a registered mortgage in favour of ASCF. Over 98% of our loans are in residential backed property with a limited number of loans over commercial property.

If you look at the average weighted loan to valuation ratio on these loans across all our retail funds they are currently at sub 60% which leaves quite a buffer. We have all heard of the term “safe as houses” well one could argue that in terms of our track record the saying applies and we don’t say that lightly.

Since inception in 2016 ASCF has funded close to $1 billion dollars in loans across the group, and no investor has ever suffered a loss, nor has our unit price declined at any point. All investor redemptions have been in full and on time and all investor interest payments have been met.

As we enter our eighth year in operation, we have paid out over $56,500,000 to investors in interest payments and whilst we are very much a boutique mortgage fund we believe that our business model has stood the test of time in ensuring our investor’s funds are well managed with capital preservation remaining our highest priority across all our portfolios, and our track record clearly evidences that.

An Interesting Transaction

Problem:

A customer was introduced to us by a valued broker seeking funding to pay out their outstanding ATO tax debt. The customer was in the process of listing their property for sale, and using the proceeds to clear the tax debt, however the ATO was putting pressure on the customer to pay immediately.

Solution:

Given the customer was intending to sell her property, ASCF was able to provide a 2nd mortgage for $320,000 at 19.8% p.a. for a term of 9 months providing the borrower sufficient time to sell property. The LVR was confirmed by a valuation at 65.88% (including the 1st mortgage).

The customer proposes to sell their property and pay us out prior to the expiry of the loan.

What ASCF Does Differently:

With only limited options in the market available to finance ATO Tax debts, ASCF takes a pragmatic approach to providing a solution to meet our clients needs.

Market Update

The first weekend of March saw 2,019 auctions take place across the combined capital cities, down slightly on the previous year’s 2,054, however clearance rates were up, 71.8% in comparison to 66.3% in 2023. Melbourne once again led the way, with 1,038 auctions taking place, followed by Sydney with 721, well above that of the other capitals, with Brisbane, Adelaide, Canberra and Perth recording 103, 85, 69 and 3 auctions respectively.

The preliminary clearance rate of 71.8% for the weekend indicates that buyers and sellers are on the same page for the most part, particularly in Sydney where a clearance rate of 76.8% was achieved, well above the 68.7% of the same weekend last year.

Melbourne, Adelaide, Brisbane and Canberra all managed to achieve clearance rates of above 60% for the weekend, with 70.1%, 69.4%, 65.0% and 63.8% respectively. It is interesting to note that all capital cities achieved a greater clearance rate than the same weekend in 2023, other than Adelaide, where a 72.9% clearance rate was achieved on the same weekend last year.

February brought yet another strong month for property prices, with CoreLogic’s Home Value Index showing a 0.6% increase across the combined capitals and combined regionals, with all capital cities experiencing growth except for Hobart, where prices fell by 0.3% for the month.

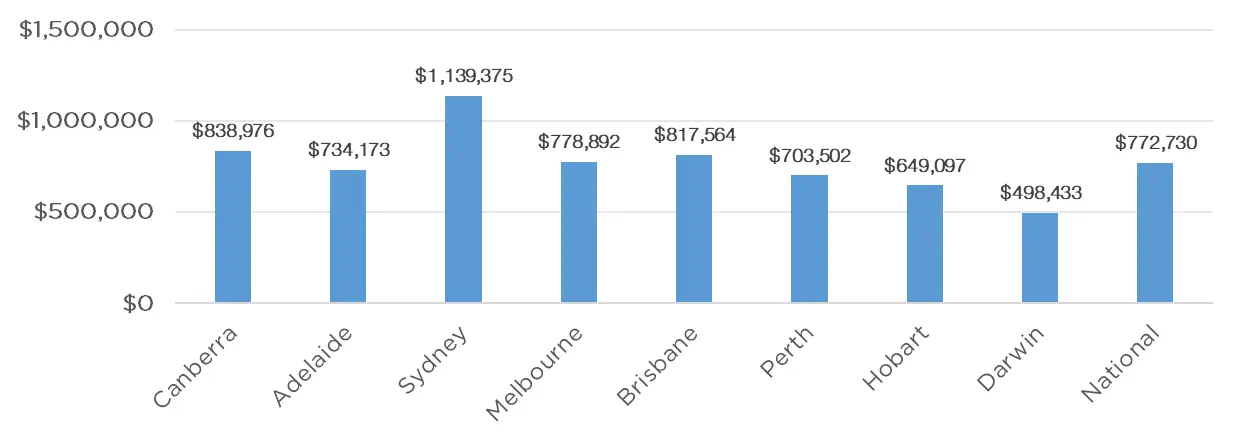

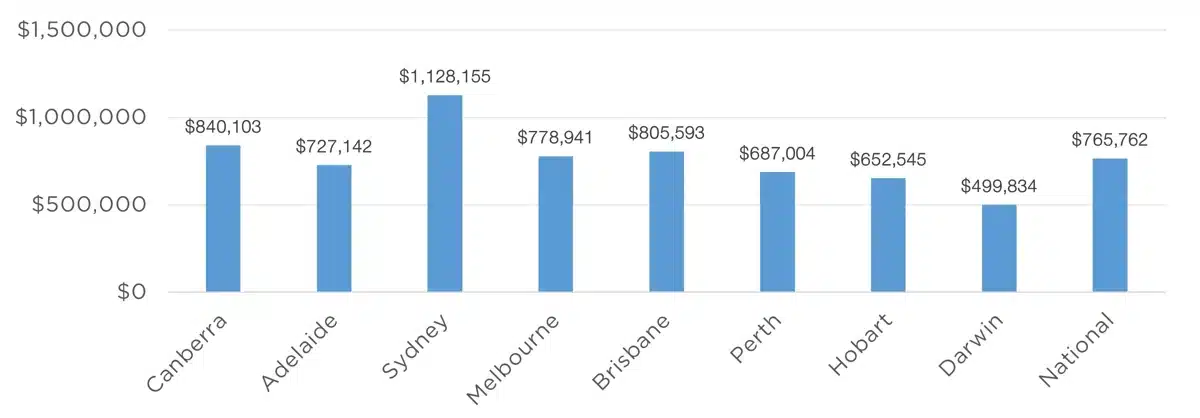

Once again, Perth experienced the greatest level of growth, increasing by a mammoth 1.8% for the month, contributing to a 5.2% quarterly growth and an increase of 18.3% annually. Adelaide also experienced strong monthly growth of 1.1%, followed by Brisbane with a further 0.9% increase, bringing the median property value of Brisbane above $800,000 for the first time, with a median value of $805,593, the second highest median value nationally, behind only Sydney with $1,128,155. Canberra, Sydney and Melbourne also experienced growth for the month of 0.7%, 0.5% and 0.1% respectively, with all cities except for Hobart (-0.6%) and Darwin (-0.1%) experiencing an annual increase.

Whilst there was no RBA meeting this month, economists continue to believe we are at the end of the rate hike cycle, with many expecting interest rate reductions before the end of 2024. Should interest rates ease, we expect that there will be a bump in property prices.

Clearance Rates & Auctions

week of 4th of March 2024

Property Values

as at 1st of March 2024

Median Dwelling Values

as at 1st of March 2024

Quick Insights

Values to Outperform

Two-fifths of valuers surveyed by CBRE have predicted house prices to outperform by up to 10% in Adelaide, Perth, and Sydney. Valuers were also relatively bullish on the apartment sector with 44 per cent predicting prices to increase over the next 12 months. The survey also highlighted a high level of demand from upgraders and downsizers, buyer segments who were less sensitive to interest rate movements.

Source: Australian Financial Review

Build-to-Rent Builds Steam

Salta Properties, is now surging into the build-to-rent sector, with ambitions to create a $3 billion platform and with its first project in inner-city Melbourne close to completion.

“We could see that we were heading into a fairly significant housing shortage in Melbourne, and more broadly across Australia,” said Sam Tarascio, manager of the firm. The first block is a 94-unit project in trendy Fitzroy North at 249 Queens Parade.

To be known as Fitzroy & Co, the building has topped out and is on track to welcome first residents from July into their one, two and three-bedroom apartments. Those tenants can expect a range of resident services, access to shared spaces and a variety of amenities.

Source: Australian Financial Review

Investor’s Update – January 2024

Trading Update

Welcome to our first newsletter for 2024!

The RBA’s decision on Tuesday to leave rates on hold was widely expected after the December quarter inflation print came in at lower than expected at 4.1%.

ASCF Current Targeted Distribution Rates

ASCF High Yield Fund

| 3 Months | 6 Months | 12 Months | 24 Months |

|---|---|---|---|

| 6.50% | 7.25% | 7.75% | 7.30% |

ASCF Select Income Fund

| 3 Months | 6 Months | 12 Months | 24 Months |

|---|---|---|---|

| 6.25% | 6.75% | 7.25% | 6.75% |

ASCF Premium Capital Fund

| 6 Months | 12 Months | 18 Months | 24 Months |

|---|---|---|---|

| 6.10% | 6.25% | 6.75% | 6.30% |

ASCF Private Fund

| 3 Months | 6 Months | 12 Months | 24 Months |

|---|---|---|---|

| 8.19% | 8.39% | 8.59% | 8.49% |

Residential property prices continue to remain resilient with Core Logic’s national Home Value Index indicating a 0.4% increase in values for January with Brisbane, Adelaide and Perth values increasing by 1% or more.

We do expect residential prices to stabilise during the course of 2024 supported by the likelihood of interest rate reductions later this year and also the ongoing reality of a structural under supply in housing across the country predominantly due to elevated migration levels.

The gross rental yield on residential property also remains stable at 3.73% nationally, supported by a 0.8% increase in rental values in January which was up from a 0.6% increase in December. The current yield is in line with the average over the last 10 years at 3.78%.

Consumer confidence remains low, however with cost of living pressures slowly starting to ease and rate reductions on the horizon we do expect this will improve during the course of 2024.

Whilst the commentary contained in the RBA statement indicated it was open to further rate raises should future data releases not be in line with their forecasts we believe inflation will continue to fall over the coming the months.

This should open the door for the RBA to cut rates later this year with most economists expecting two rate reductions of 0.25% each which would bring the cash rate back down to 3.85% by year end.

Monthly Managed Fund Cumulative Growth & Performance

Note 2: Past performance is not indicative of future performance

Managed Funds Under Management

as at 31st of January 2024

| January 2024 | |

|---|---|

| ASCF High Yield Fund | $137,303,003.97 |

| ASCF Select Income Fund | $45,408,687.73 |

| ASCF Premium Capital Fund | $23,083,853.82 |

| Combined Funds under Management | $205,795,545.52 |

In January, loan originations and inquiry levels remained solid, with $7,997,814.00 in new loan originations settled.

The unit price across all three of our retail funds remains stable at $1.00 per unit.

All monthly distributions have been paid in full for the month of January.

Lending Activity Update

Quarterly Loan Settlements

as at 31st of January 2024

Current Loans by Fund Source

as at 31st of January 2024

| High Yield Fund | Select Income Fund | Premium Capital Fund | |

|---|---|---|---|

| 1st Mortgage Loans | 81.08% | 100% | 100% |

| 2nd Mortgage Loans | 12.63% | 0% | 0% |

| 1st & 2nd Mortgage Loans | 6.29% | 0% | 0% |

| Avg. Weighted LVR | 54.06% | 54.16% | 46.05% |

| Avg. Loan Size | $1,368,807.43 | $1,142,474.06 | $737,589.29 |

Current Loans Geography

as at 31st of January 2024

Why Invest with ASCF?

Private credit is now flourishing in most overseas markets and the uptake of Australian investors into an asset class that can move with interest rates, beat the inflationary pressures on their cash and assist with rising cost of living by generating consistent returns is now becoming more prevalent.

But what makes ASCF different from other mortgage funds?

- We don’t fund risky construction loans. ASCF does not provide construction loans to property developers, that is we only lend on the as is value of the asset at the time of the loan.

- Over 95% of our loan book across all our funds is in residential loans, we rarely lend on commercial properties.

- We are a short term lender, with an average weighted loan term of around 9 months. This makes our funds very liquid and as the property market moves our loan book resets based on the movements in the market.

- Our targeted distribution rates are set for the duration of your investment, so if you invest with us now your rate will not fluctuate during the course of your investment term should the RBA reduce rates during your term.

- Capital preservation. Since inception we have funded close to $1B in loans across all ASCF funds and no investor has ever suffered any loss, and all interest distributions and investor redemptions have been paid on time and in full.

Whilst past performance is not indicative of future performance, we believe our record speaks for itself so if you are looking for an inflation response investment with capital stability we believe an investment in our ASCF High Yield Fund which is currently paying 7.75% p.a for a 12 month investment term is definitely worth considering.

An Interesting Transaction

Problem:

A repeat ASCF borrower was completing renovations to an investment property and required a further $200,000 to complete the renovations before placing it on the market for immediate sale. Their current lender refused to increase their 1st mortgage due to the short term nature of the loan. ASCF obtained a valuation report which provided an ‘as is’ valuation of the property.

Solution:

Based on the valuation figure, ASCF was able to lend sufficient funds for the borrowers to pay out their first mortgage, and complete their renovations. ASCF provided a gross loan amount of $500,000, including capitalised interest, at an LVR of 52.63% and an annual rate of 13.80%.

Our loan provides a six-month term which allows sufficient time for the renovations to be completed and the property to be marketed and sold.

What ASCF Does Differently:

ASCF is a specialist in providing short term loans to borrowers so they can meet their objectives when traditional lenders refuse to assist borrowers in meeting their short term goals.

Market Update

The first RBA meeting of the year has taken place, with the cash rate remaining on hold at 4.35%. Recent inflation data has given economists confidence that we have reached the end of the rate hike cycle.

The first weekend of February brought the start of the 2024 auction season, with a mammoth 1,671 auctions being held across the combined capitals. This is the second largest opening weekend since 2008, with only the corresponding weekend in 2022 holding more auctions, with 1,779 taking place.

This result was up 26.4% on 2023 data, and was more than double than double the number of auctions held over the year so far (803). Melbourne recorded the most auctions for the weekend, with 603 taking place, followed closely by Sydney with 562. Brisbane, Adelaide and Canberra also recorded triple digit auction numbers with 203, 159 and 132 auctions taking place respectively, whilst Perth and Tasmania held just 9 and 3 auctions respectively.

Preliminary clearance rates have also begun the season strongly, with a clearance rate of 73.9% across the combined capital cities, well above the 61.9% of 2023. Canberra led the way with 80.0%, followed by Adelaide, Sydney and Melbourne with 77.6%, 76.3% and 71.9% respectively. Brisbane being the only capital below 70% with a 68.5% result.

The property market continues to show growth, albeit signs of cooling do exist, with a 0.4% increase across both the combined capitals and regionals.

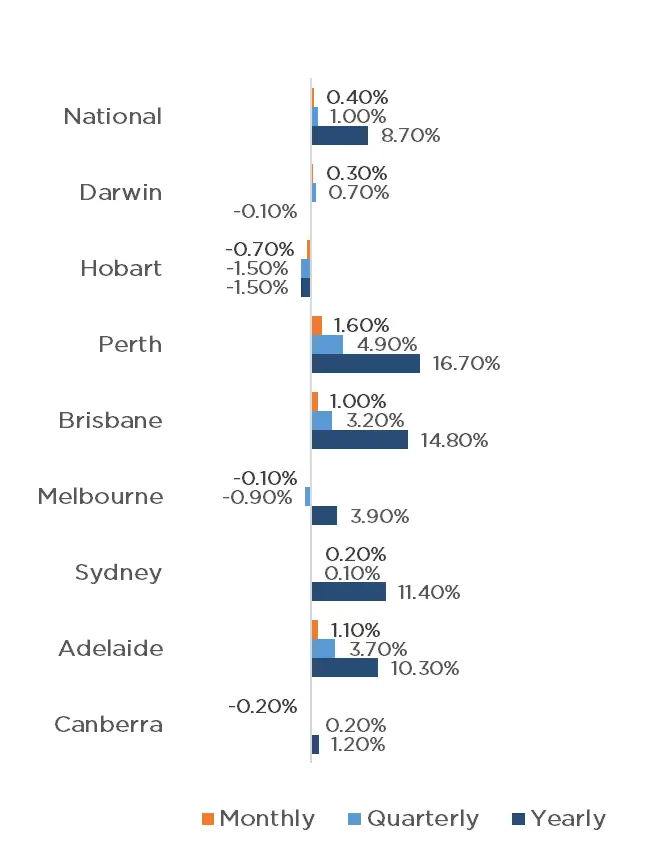

Perth continues to experience the highest rate of growth, increasing by 1.6% for January, followed by Adelaide and Brisbane with 1.1% and 1% respectively. Darwin and Sydney also experienced growth of 0.3% and 0.2% respectively, whilst prices in Melbourne, Canberra and Hobart have fallen by 0.1%, 0.2% and 0.7% respectively. The annual change remains significant with a 10% increase across the combined capitals, and 4.9% increase for regional centers, contributing to a national increase of 8.70%.

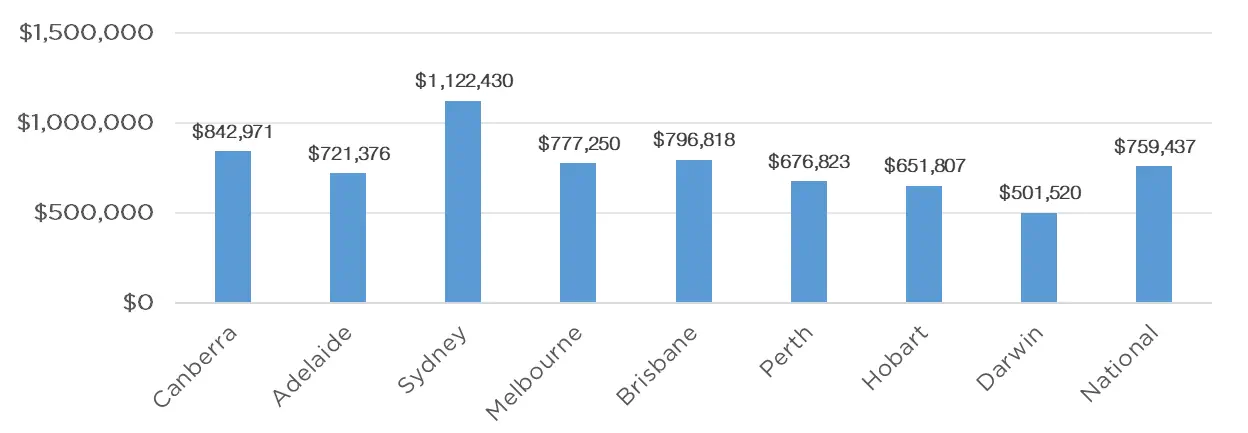

This has been driven by four of the capitals experiencing double figure growth with 16.70% for Perth, 14.80% for Brisbane, 11.40% for Sydney and 10.30% for Adelaide. Melbourne and Canberra also recorded growth for the year with 3.90% and 1.20% whilst only Darwin and Hobart saw prices fall for the year with 0.1% and 0.4% respectively. This has led to Brisbane now holding the second highest median value in the country, overtaking Melbourne with a median value of $796,818 compared to Melbourne’s $777,250.

Whilst the property market has begun to show signs of easing, given that economists predict we are at the end of the rate hike cycle, we anticipate that property prices will still experience growth throughout 2024, as interest rates begin to subside, and the lack of housing supply continues.

Clearance Rates & Auctions

week of 4th of February 2024

Property Values

as at 1st of February 2024

Median Dwelling Values

as at 1st of February 2024

Quick Insights

Will Values Fall? Unlikely.

With home values in capitals such as Sydney still 2.4% lower than their peaks, many investors such as Sydney-based investor Nicholas Marangos-Gilks are more motivated than ever to increase demand in the market. Buyers are not waiting for the rate cut to occur.

Tim Lawless, CoreLogic research director, has commented, “We are still seeing housing values below their record highs in Sydney, Melbourne, Hobart, Darwin and the ACT. In these cities we could see motivation from buyers looking to get into the market while values are still below their peaks.”

Source: Australian Financial Review

Looser Planning, not Restrictive Taxes

Eliminating negative gearing and ditching capital gains tax discounts will not solve the worsening housing affordability crisis, but boosting supply by easing planning rules will, a new report says.

Centre for Independent Studies chief economist and former Reserve Bank official Peter Tulip said restrictive planning rules have added more than 40% to house prices in Sydney and Melbourne, while property taxes boosted values by 4% at most.

“There are arguments from the tax policy perspective that negative gearing and the capital gains discount should be considered, but it’s not relevant to the question of housing affordibility,” he said.

Source: Australian Financial Review

Investor’s Update – November 2023

Trading Update

The RBA’s decision to leave rates on hold last week was very much as expected based on the October monthly inflation data which came in at 4.9% on an annual basis compared to September which was running at 5.6%.

The inflation data combined with the release of September’s GDP data at 0.2% which is well below forecasts of 0.4% clearly indicate that the impact of the RBA’s tightening policy it embarked on last year is working to take the heat out of the economy and bring inflation back within its 2-3% target.

Markets are now expecting the RBA to start cutting rates from mid to late next year and are fully pricing in a rate cut of 25 basis points and a 50% chance of rates dropping by 50 basis points by the end of 2024.

ASCF Current Targeted Distribution Rates

ASCF High Yield Fund

| 3 Months | 6 Months | 12 Months | 24 Months |

|---|---|---|---|

| 6.50% | 7.25% | 7.75% | 7.30% |

ASCF Select Income Fund

| 3 Months | 6 Months | 12 Months | 24 Months |

|---|---|---|---|

| 6.25% | 6.75% | 7.25% | 6.75% |

ASCF Premium Capital Fund

| 6 Months | 12 Months | 18 Months | 24 Months |

|---|---|---|---|

| 6.10% | 6.25% | 6.75% | 6.30% |

ASCF Private Fund

| 3 Months | 6 Months | 12 Months | 24 Months |

|---|---|---|---|

| 8.19% | 8.39% | 8.59% | 8.49% |

With the next RBA meeting not scheduled until February next year it should provide mortgage holders some welcome relief however the December quarter inflation print released at the end of January will be paramount in the RBA’s decision.

Whilst we believe rates will come down next year and through 2025 the pace at which the RBA cuts rates will be measured and with current economic forecasts indicating rate reductions of anywhere between 0.75% and 1.5% by March 2026 we are clearly at the top of the cycle.

Residential property prices across the nation are now starting to flatline, and we expect limited gains moving forward although we believe they will continue to be supported by the structural undersupply of housing so we do not expect any significant declines.

In fact we believe that overall 2024 will be a positive year for residential property nationally particularly as the possibility of rate reductions become more evident to buyers from mid 2024.

As this is our final newsletter for 2023, we would like to wish you all a Merry Christmas and Happy New Year from all of us at ASCF.

Our next newsletter will be issued in February 2024.

Monthly Managed Fund Cumulative Growth & Performance

Note 2: Past performance is not indicative of future performance

Managed Funds Under Management

as at 30th of November 2023

| November 2023 | |

|---|---|

| ASCF High Yield Fund | $132,342,341.97 |

| ASCF Select Income Fund | $44,474,407.73 |

| ASCF Premium Capital Fund | $26,558,853.82 |

| Combined Funds under Management | $203,375,603.52 |

In November, loan originations and inquiry levels remained solid, with $8,973,468.50 in new loan originations settled.

The unit price across all three of our retail funds remains stable at $1.00 per unit.

All monthly distributions have been paid in full for the month of November.

Lending Activity Update

Quarterly Loan Settlements

as at 30th of November 2023

Current Loans by Fund Source

as at 30th of November 2023

| High Yield Fund | Select Income Fund | Premium Capital Fund | |

|---|---|---|---|

| 1st Mortgage Loans | 80.53% | 100% | 100% |

| 2nd Mortgage Loans | 13.53% | 0% | 0% |

| 1st & 2nd Mortgage Loans | 5.94% | 0% | 0% |

| Avg. Weighted LVR | 54.58% | 60.43% | 43.75% |

| Avg. Loan Size | $1,397,605.71 | $1,119,452.00 | $732,676.84 |

Current Loans Geography

as at 30th of November 2023

Why Invest with ASCF?

There’s a saying that inflation is a tax against your savings, and this is very true. When the value of currency goes down, the ‘buying power’ of the money you’ve saved also goes down. Thus, while you have the same amount of money, you are, in effect, worse off.

There is another popular saying that is “don’t save your money, invest it”. It’s pretty obvious that the investment needs to be returning a higher rate than the rate of inflation i.e. if the inflation rate is 5% you need your investments to be making more than 5%, otherwise you are just going backwards. To keep ahead of the curve, an investor must be able to grow their money faster than the effects of inflation.

So how can investors keep ahead of the curve to protect themselves from the effects of inflation and what should you do during inflationary periods?

Steer clear of having your funds invested in cash or in a savings account that is paying a rate of less than the rate of inflation. The reason for this is that inflation is linked to rising prices. If you have $100 in your wallet now, you can buy a certain amount of goods or services. If inflation pushes the price of those products up to $110 next year, you won’t be able to buy as much with your $100. If you hold this money in a bank account that pays no or little interest, the result is the same.

Another example is if your bank pays you 4% interest on your savings but inflation is 5%. So the real interest rate for your savings is -1%, which means your purchasing power will decrease by 1% per year and you are going backwards.

Look for investment options returning above inflation rates.

Whilst the returns are not guaranteed, there are options out there that will be offering above inflation returns.

However, not all investments are the same. Some require more attention than others, while some, by their nature, require huge capital upfront. Understanding your current situation and investor profile is crucial when selecting which investments match your financial goals. Otherwise, you could end up suffering big losses instead of gaining additional income.

Markets will always have highs and lows. What’s important is that the general trajectory is moving in your favour in the long term.

Research and ask as many questions until you are satisfied. Investing should protect you from inflation, not compound the problem because you entered into something you didn’t completely understand.

Our High Yield fund is now paying a targeted return of 7.75% p.a. for a 12 month investment or 7.30% p.a. for a 24 month investment with interest paid monthly and definitely worth considering if you are seeking a low volatility inflation responsive investment over the next 12 to 24 months.

Now is a great time to invest in one of our term investments knowing that the rate will be fixed for the duration of the investment term regardless of whether rates start to fall later next year.

An Interesting Transaction

Problem:

A

A broker was struggling to find a funder willing to assist with a client’s urgent off-the-plan purchase.

The client had signed contract in March 2021 to purchase a unit off the plan in Mermaid Beach, Gold Coast for $1.63m. Construction had been completed, titles issued and the developer then called for settlement within 14 days. The problem the client faced was that she had not yet sold her principal place of residence or her investment property to be able to purchase the unit. The broker tried to get urgent funding from a second-tier lender, but not only were they unable to settle in time, the client’s husband had recently passed away, so the second tier-lender was not able to lend against her existing properties or demonstrate servicing. Further, the value of the new unit had increased to $2.65m since the contract date so the client faced losing a $1m uplift if she failed to settle, along with losing her 10% deposit!

Solution:

A broker that regularly deals with ASCF suggested the broker contact their ASCF relationship manager. ASCF was able to provide a bridging facility of $1,730,000 to ensure the client had sufficient funds to complete the purchase before the contract was terminated by the developer. By taking advantage of the equity the client had in their existing properties, ASCF was able to provide the funds at an LVR of 40.71% at the rate of 11.95% p.a.

The loan provided a six-month term which allowed more than sufficient time for the client to sell her existing properties and exit the ASCF loan.

What ASCF Does Differently:

An excellent example of how ASCF is able to provide a positive outcome for its borrowers by utilising a common-sense approach and overcoming obstacles banks often fail to see-through.

Market Update

Christmas came early for mortgage holders and new borrowers when the RBA left interest rates on hold at the December meeting. This hold, means the cash rate will remain at 4.35% until at least February, with no meeting taking place in January, providing reprieve for mortgage holders over the holiday period.

The first week of summer saw strong auction activity across the capitals with 2,999 auctions taking place, headlined by Melbourne and Sydney with 1,380 and 1,112 auctions respectively. Adelaide, Brisbane and Canberra all recorded triple digit auction figures with 190, 178 and 120 auctions respectively, whilst there were 17 in Perth and 2 in Tasmania.

Preliminary clearance rates are trending lower, with 67% of auctions being successful. Once again, Adelaide recorded the highest clearance rate with 77.4%, followed closely by Brisbane with 76.1%, with just the two capitals achieving a clearance rate of over 70%. Sydney and Melbourne both recorded clearance rates of above 60% with 68.5% and 64.6% respectively, whilst Canberra and Perth received a clearance rate of 55.1% and 46.2% respectively.

The rapid rise of the property market has shown signs of cooling, with CoreLogic’s National Home Value Index showing a smaller, 0.6% increase for the month, reaching a new record high.

Perth recorded the largest monthly gain since March 2021, with 1.9%, followed by Brisbane and Adelaide with 1.3% and 1.2% respectively. Canberra and Sydney were the only other two capitals to achieve an increase, growing by 0.5% and 0.3% respectively, whilst Melbourne and Hobart both recorded a reduction of 0.1%, Darwin had a negative result with a 0.3% reduction.

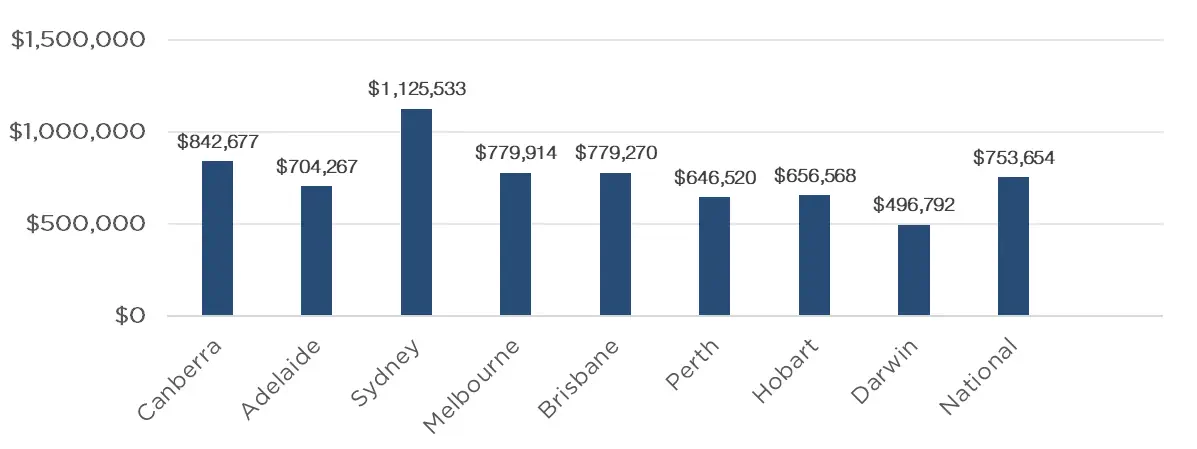

As the Brisbane property market continues to flourish, the average dwelling value in Melbourne is now less than $700 greater than that of Brisbane ($779,914 and $779,270 respectively) and may see Brisbane become the second most expensive capital city in a matter of weeks.

The pause in the cash rate has eased pressure leading into the holiday season. Inflation and employment data over the coming months will go a long way in determining the outcome of the February RBA meeting, however regardless of the result, the property market remains strong, continuing to be driven by a fundamental lack of supply, and an influx in migration to Australia.

Clearance Rates & Auctions

week of 4th of December 2023

Property Values

as at 1st of December 2023

Median Dwelling Values

as at 1st of December 2023

Quick Insights

House Price Soars Despite the Flights

A property in the Sydney suburb of Mascot has sold for over $1.65 million despite its close proximity to Sydney Airport.

After selling for $50,000 over reserve, the agent said, “The buyers just forgot about the aeroplanes. They bought it based on what they could buy for that price and live in Sydney. Despite the planes – you could touch their wheels – the buyers came back three, four, five times.“

Source: Australian Financial Review

Populism & Property Taxes

The Labor federal government has recently announced a plan to triple the foreign investment fee for purchases of established homes and to double the vacancy fee for homes owned by overseas investors.

While interest in buying Australian residential property by China-based buyers is increasing, Real Estate Institute of Australia president Leanne Pilkington said they would make little difference.

AMP chief economist Shane Oliver said: “It’s something that is populist policy, foreigners are not the cause of the problem. We went through the pandemic and there were no foreigners buying property and prices still took off.”

Source: Australian Financial Review

Investor’s Update – October 2023

Trading Update

We are pleased to advise that we have increased our targeted distribution rates across all our funds.

The rates for the 3, 6 and 12 month investment terms have been increased by 0.25% per annum and the 24 month rates have increased by 0.1% per annum.

We are also pleased to advise that we have increased our targeted distribution rates in our ASCF Private Fund, this fund is open to wholesale and sophisticated investors.

The 6, 12 and 18 month term investments in this fund have increased by 0.30%.

The rate increases across all funds will apply to all new investments and existing investments will receive the benefit of the new rates as the investments roll over on their respective maturity dates.

ASCF Current Targeted Distribution Rates

ASCF High Yield Fund

| 3 Months | 6 Months | 12 Months | 24 Months |

|---|---|---|---|

| 6.50% | 7.25% | 7.75% | 7.30% |

ASCF Select Income Fund

| 3 Months | 6 Months | 12 Months | 24 Months |

|---|---|---|---|

| 6.25% | 6.75% | 7.25% | 6.75% |

ASCF Premium Capital Fund

| 6 Months | 12 Months | 18 Months | 24 Months |

|---|---|---|---|

| 6.10% | 6.25% | 6.75% | 6.30% |

ASCF Private Fund

| 3 Months | 6 Months | 12 Months | 24 Months |

|---|---|---|---|

| 8.19% | 8.39% | 8.59% | 8.49% |

The new RBA governor has certainly showed her hand in terms of how she intends to ensure inflation comes back within the RBA target band of 2% – 3% by 2025.

We still believe we are likely to hit the target by the end of 2024 with rate reductions still likely next year and whilst the September quarter inflation print was slightly above consensus we believe the downward trend remains intact and will become evident in the subsequent quarterly data releases.

The increased levels of overseas migration are obviously having a positive impact on the economy and helping to fill the post Covid job vacancies but they are also adding to inflation pressures in terms of housing and increased spending generally.

Money markets are currently indicating that the chances of a further rate rise are less than 50% but this will now obviously be data dependent and if one thing became evident from last week’s decision its that the RBA is more likely to move quickly should any subsequent quarterly inflation prints not be in line with their current estimates.

The rate increase did little to impact the auction clearance rates with the average across all capital cities holding up well at 68.6% and 63.1% respectively for the first two weekends post the RBA decision. Whilst unemployment remains low and governments struggle to implement policies that will help with the structural undersupply of housing across the country we do not believe the most recent interest rate rise will overly impact property prices however it may temper the month on month growth we have seen over the last several months.

Monthly Managed Fund Cumulative Growth & Performance

Note 2: Past performance is not indicative of future performance

Managed Funds Under Management

as at 31st of October 2023

| September 2023 | |

|---|---|

| ASCF High Yield Fund | $130,469,121.97 |

| ASCF Select Income Fund | $44,129,618.73 |

| ASCF Premium Capital Fund | $26,461,353.82 |

| Combined Funds under Management | $201,060,094.52 |

In October, loan originations and inquiry levels remained solid, with $11,861,352.73 in new loan originations settled.

The unit price across all three of our retail funds remains stable at $1.00 per unit.

All monthly distributions have been paid in full for the month of October.

Lending Activity Update

Quarterly Loan Settlements

as at 31st of October 2023

Current Loans by Fund Source

as at 31st of October 2023

| High Yield Fund | Select Income Fund | Premium Capital Fund | |

|---|---|---|---|

| 1st Mortgage Loans | 81.87% | 100% | 100% |

| 2nd Mortgage Loans | 14.76% | 0% | 0% |

| 1st & 2nd Mortgage Loans | 3.37% | 0% | 0% |

| Avg. Weighted LVR | 55.11% | 60.43% | 43.75% |

| Avg. Loan Size | $1,446,452.63 | $1,181,291.67 | $700,476.49 |

Current Loans Geography

as at 31st of October 2023

YEARLY AUDITED FINANCIALS ARE NOW ONLINE

We are pleased to advise that ASCF’s full year audited 2023 Financial Statements and Compliance Audit Reports for ASCF Premium Capital Fund, ASCF Select Income Fund and ASCF High Yield Fund are now available to download from our website.

You can view the financials by clicking here.

Should you have any questions in relation to the financials, please do not hesitate to contact our Investor Relations team on 1300 269 419.

2023 TAX CERTIFICATES NOW AVAILABLE

Tax Certificates for financial year ending 30th June 2023 are available to download via our online portal. If you are not registered for the portal, please contact us on 07 3506 3690 and our friendly team will assist you through the registration process.

Make sure you have the mobile phone associated with your account handy, as it will be needed during the registration process.

Need help?

Please contact us:

[email protected]

07 3506 3690

Monday – Friday 9am – 5pm AEST

Why Invest with ASCF?

ASCF is one of Australia’s leading short-term mortgage lenders, our objective is to provide consistent, high yielding investment returns that are secured by quality Australian real estate assets. All of our loans are by way of a registered mortgage over Australian residential, vacant land and/or commercial property, we do not do any construction loans, property development loans, high rise apartment loans, unsecured personal loans, car loans or equipment finance.

One of the ways ASCF continues to grow and thrive is because of how we effectively manage liquidity – at any one time we usually hold between 5% and 10% of the value of the Fund in liquid assets to cover withdrawals, monthly distributions and expenses.

Investing in a mortgage fund that effectively manages its liquidity can offer several advantages to investors. Liquidity management is crucial for such funds to ensure they can meet redemptions and seize investment opportunities while minimising risks. Here are five advantages for an investor in a mortgage fund that properly manages its liquidity:

Reduced Redemption Risk: When a mortgage fund manages its liquidity well, it is better prepared to meet redemption requests from investors without having to liquidate its loan book. This reduces the risk of forced liquidations, which could lead to losses for investors.

Stable Returns: Effective liquidity management can help the fund maintain a more stable portfolio, which, in turn, can lead to more predictable returns for investors. Avoiding sudden disruptions due to liquidity issues can contribute to a smoother investment experience. ASCF has a proud record of ensuring the value of investors’ initial investment has remained stable at $1.00 per unit since inception.

Capital Preservation: Proper liquidity management ensures that the fund retains enough cash or highly liquid assets to cover short-term obligations. This helps protect investors’ capital and ensures that they are less exposed to unexpected losses. None of our investors has ever lost any of their capital by investing in any of the three ASCF Mortgage Funds.

Enhanced Yield Opportunities: With adequate liquidity at its disposal, a mortgage fund can take advantage of attractive investment opportunities as they arise. This agility can lead to higher yields and potentially improved returns for investors.

Risk Mitigation: Liquidity management is a key aspect of risk management. A fund that handles liquidity effectively is better positioned to navigate market volatility, economic downturns, or unexpected events, reducing overall risk exposure for investors.

It’s important for investors to carefully assess a mortgage fund’s liquidity management strategy and policies before investing, as this can have a significant impact on the fund’s performance and their own investment outcomes.

An Interesting Transaction

Problem:

A valued broker introduced a consortium of professional individuals to ASCF seeking funding to refinance an existing loan secured by a development approved subdivision of land in Mount Cottrell, in Victoria.

Solution:

Our valuation confirmed an LVR of 65.22% against the property and we provided a 12 month facility for $3m with interest prepaid for the first 6 months at a rate of 11.95% pa. We were also able to take collateral mortgages over two residential properties to strengthen our security position.

The borrower will repay the loan from the sale of the site or via refinance through a construction facility.

What ASCF Does Differently:

Another example of how ASCF is able to assist its customers in executing on their wealth creation strategies.

Market Update

The November RBA meeting brought the 13th interest rate increase for the cycle, raising rates by 25 basis points, bringing the cash rate to 4.35%. This increase was anticipated following the uptick in inflation as reported in the last monthly newsletter.

The first weekend of November saw a week-on-week reduction in auctions of 40% in the lead up to the Melbourne Cup with 2,015 auctions taking place. This was however somewhat expected following the “Super Saturday” auction in October, with 3,381 auctions being held over a single weekend.

Sydney held the most auctions by a considerable margin, with 1,065 well above that of Melbourne with 453. Adelaide, Brisbane and Canberra all recorded similar figures with 181, 150 and 144 respectively, whilst Perth recorded just 18 auctions for the weekend.

The uncertainty surrounding interest rates marginally impacted clearance rates, with the clearance rate falling to 68.6% for the weekend, despite the lower levels of stock. This was evident with just Adelaide and Sydney recording above a 70% clearance rate with 74.8% and 71.9% respectively. Brisbane was not far behind with 68.6%, so too with Canberra at 67.7%. Melbourne was well below however, with a clearance rate of just 60.8% for the weekend.

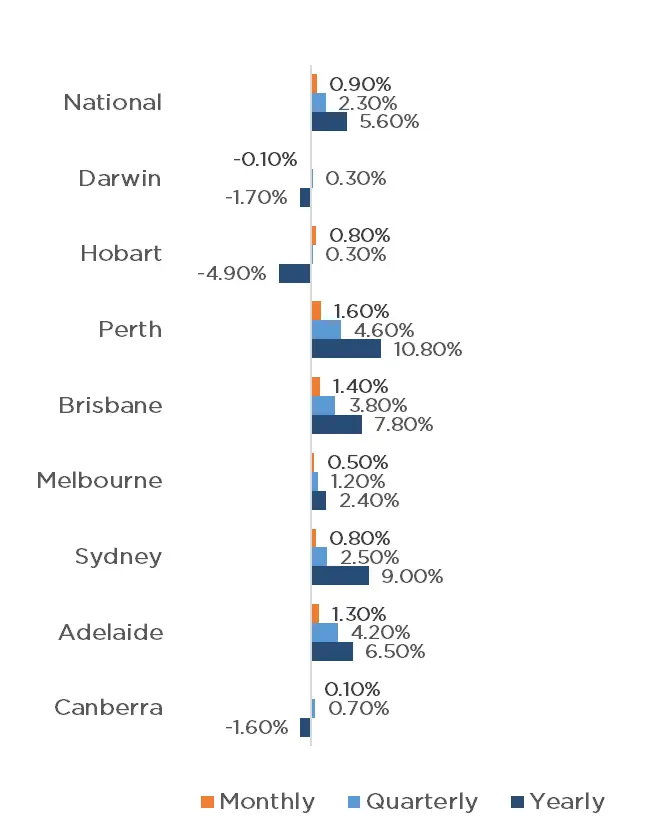

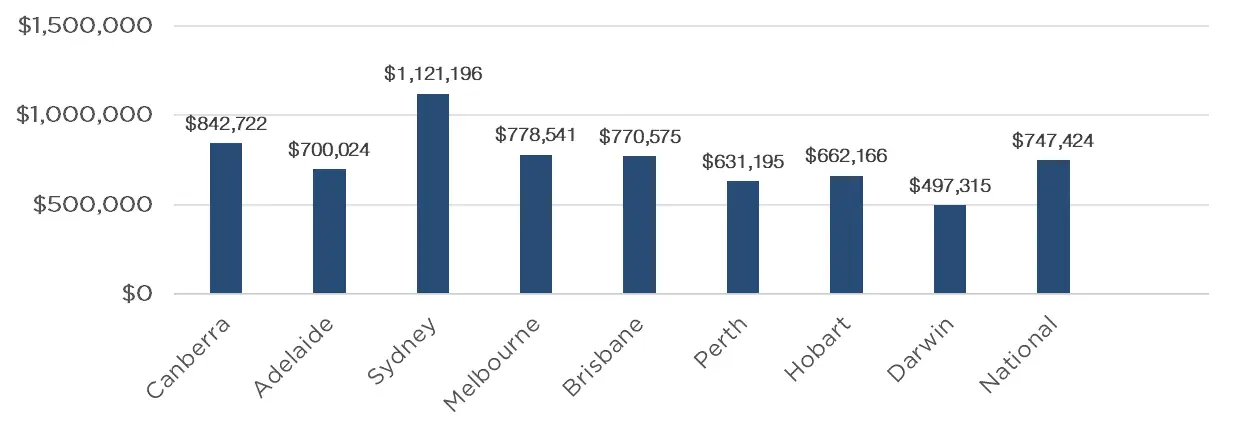

CoreLogic’s national Home Value Index rose a further 0.9% in October, which could see property prices reach a new record high before the end of year if the trend continues. This was driven by strong growth above 1% in 3 capital cities with Perth recording the largest monthly increase with 1.6%, followed by Brisbane and Adelaide with 1.4% and 1.3% respectively. Sydney (0.8%), Hobart (0.8%), Melbourne (0.5%) and Canberra (0.1%) all recorded growth, with just Darwin recording a loss (0.1%) for the month. With the continued strong growth of Brisbane, average dwelling prices are nearing that of Melbourne with less than $8,000 separating the two cities ($770,575 and $778,541 respectively).

Whilst most economists predicted the RBA to dampen Cup Day celebrations with a rate increase, there are mixed opinions on whether we have reached the peak. With rates already being well above economist predictions from earlier in the year, and mortgage holders feeling the pinch, a further rate rise may deter potential buyers and take the heat out of the property market, reducing the current growth rate.

Clearance Rates & Auctions

week of 12th of November 2023

Property Values

as at 1st of November 2023

Median Dwelling Values

as at 1st of November 2023

Quick Insights

Economists Stand Ground as Cash Rates Rise

Despite the rise in rates this month from the RBA economists remain resolute that any downturn is likely to be a short slowdown rather than a crash.

PEXA chief economist Julie Toth said, “We may see a welcome pause in price increases, but I doubt we’ll see another fall. On the flipside, we’ll probably see a burst of activity in refinancing.”

Source: Australian Financial Review

Growth, Growth, & More Growth

According to a survey of 10 economists and analysts conducted by The Australian Financial Review, many are expecting a 6.50% – 8.00% rise in property prices by 2024.

Jarden chief economist Carlos Cacho said, “The key drivers of this increase are expected to be continued limited listings, particularly of family homes, along with positive sentiment towards housing, given households’ expectations of RBA easing next year. That said, we don’t expect rate cuts until late 2024, at the earliest, which may challenge this positive sentiment.”

Source: Australian Financial Review

Lend Leasing in Australia

Land Lease arrrangements where a property owner owns the phyysical structure but rents the land it sits on are becomeing increasingly common in Australia with over 10,000 development under way and another 15,000 in the pipeline.

Residents say they are safer, more connected to community, and better off financially. They have become of particular interest to older Australians who need to downsize.

Source: Australian Financial Review